Buy / Sell Business Succession Cover

Protection for transfer of business ownership

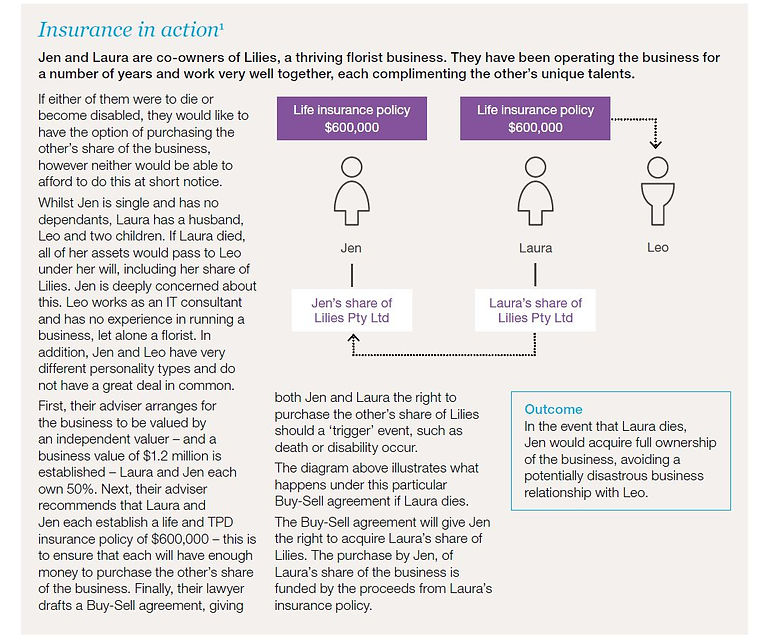

You may share the ownership of your business with one or more people. If you do, it may be important to consider what would happen to the ownership of the business if one of the owners died or had to exit.

Business owners will sometimes establish a legal agreement, such as a Buy-Sell agreement in order to provide more certainty if this happens.

A Buy-Sell agreement is a document which commonly sets out the wishes of the business owners should one of them die, become incapacitated or trigger any one of a range of specified events. It can be drafted in a number of ways to suit your circumstances and those of your business. For example, if your business partner dies, a Buy-Sell agreement can be structured to give you the legal right to buy their share of the business for a specified amount. The agreement could also give you (or your beneficiaries) the right to sell your share of the business to the other business owner(s), should one of these events happen to you. The purchase can be funded by life insurance policies, taken out on the lives of each owner.

A Buy-Sell agreement coupled with an insurance policy can be useful for a number of reasons:

> If an owner dies, you may not want to work with their spouse or partner, but you may have no choice if he or she inherits the deceased owner’s share of the business and wants to manage the business with you.

> Alternatively you may want to buy that owner’s share of the business on their death or disablement, but may not be able to afford it. The spouse may then sell the business share to a third party who you may not want to work with either.

> The agreement can also set out a business valuation, helping you to avoid arguments about the value of the exiting owner’s share.

> The insurance policy can be structured so it provides the funding that allows the surviving owner(s) to purchase the exiting owner’s share and retain 100% ownership of the business.

Note: It is important to understand all of the implications of entering into a Buy-Sell agreement, including that the agreement may compel you, or your estate, to sell your share of the business. You should always seek professional legal and tax advice.

Who owns the insurance policy?

The insurance policy under a Buy-Sell agreement can be owned in a number of ways. Below is a brief description of the most common ownership methods.

Self Ownership

Self ownership involves each owner holding an insurance policy over their own life – the premium expense can either be shared, or each owner can pay their own premium. When an owner dies or becomes disabled, the Buy-Sell agreement can be structured so as to reduce the amount that the surviving owner must pay to acquire the departing owner’s share by the insurance proceeds paid from the departing owner’s policy. This helps the surviving owner to afford the purchase of the departing owner’s share – the transaction will be partially or wholly funded by the insurance policy.

Cross Ownership

Cross ownership involves the business owners holding an insurance policy over each other’s lives. The Buy-Sell agreement can be structured so that the insurance proceeds are used to help fund the transfer of business ownership. This structure is not as common as self ownership because Capital Gains Tax (CGT) is generally payable on any Total and Permanent Disablement (TPD) or Living insurance proceeds, unless the owners are defined relatives (see Taxation section).

Superannuation Ownership

Under superannuation ownership the life insurance policy is held through a superannuation fund. Superannuation ownership can potentially be tax effective but it can also create complexity, due to limits on contributions and restrictions on payments. There may also be tax consequences at the time of claim, especially where death benefits are paid to non-dependant beneficiaries such as adult children. Buy/sell insurance can not be established inside a self managed super fund.

Company Ownership

When the insurance policy is owned by a company, the proceeds from a death, TPD or Living insurance claim may be used by the company to buy back the departing owner’s shares. The result is that the remaining owners will hold a greater percentage share in the business. Under this ownership structure, CGT is generally payable by the company on the proceeds from TPD or Living insurance policies.

Trust Ownership

As an alternative to the above options, the insurance policy could be owned through a discretionary trust. The trustee will then distribute any insurance proceeds in accordance with the trust deed. Trust ownership is complex and therefore professional taxation and legal

advice is essential.

Legal and taxation advice is critical when deciding on ownership as each structure will have different tax, stamp duty and legal implications.

Who pays the premiums?

Generally speaking, the person or entity that owns the insurance policy will pay the premiums, though in some cases the owner and payer will be different. Advice is essential in this area, especially for complex business structures involving multiple entities.

An issue that may need to be considered is how the cost of premiums is allocated where the business owners differ in age and health. Because these factors can affect the cost of insurance premiums, one owner may need to pay significantly more than the other owner, for the same amount of insurance cover.

Example:

Let’s revisit Laura and Jen from the above case study. Due to Laura’s age, her premiums are 20% higher than Jen’s. Laura and Jen have a number of options for payment, including:

> sharing the cost of the total premiums, and

> each paying their own premium amount.

Advice is critical in this area and you should discuss these options with your financial adviser and professional tax adviser.

Valuing your business

If you were to sell your business today, what price would you ask for it? If you were to buy your business partner’s share of the business, how much would you pay?

Valuing your business is an essential part of business succession planning. A proper valuation can reduce the likelihood of potentially awkward or unfair negotiations on price, or even disputes with an exiting business partner or their beneficiaries.

A proper valuation can also give the parties to the agreement and their beneficiaries, much greater clarity about what their interest in the business is worth and how much they would need to pay to purchase an outgoing owner’s share.

Below are two examples of different valuation methods:

> An independent valuation performed by an accountant or qualified valuer – the method used can differ depending on the type of business and also its maturity. For example, a business that has just started will normally be valued in a different way to a business

that has been trading for a number of years.

> Agreed value – the business owners agree on a valuation between themselves. For example, you may have a good idea about how much your business is worth, and agree with your business partner on a fixed price you will pay for their share if they exit the business. However, care should be taken with this approach to ensure that the valuation can be commercially justified. Without a proper independent valuation, arguments can still arise between you and the beneficiaries of your business partner.

It is generally a good idea to update the valuation each year, or when the circumstances of the business change. A regularly updated valuation may reduce the risk of disagreements and help enable a smooth transfer.

It is also important that you see your financial adviser regularly, as changes in the valuation of the business will normally require a corresponding change to the amount of cover in your insurance policies. Without this adjustment, there can be a gap between the value of the business to be transferred and the amount of insurance cover to pay for it.

The importance of advice

Strategies to transfer business ownership can be complex and the needs of each business and its owners will be different. It is important that you seek taxation and legal advice from a professional tax adviser and suitably qualified lawyer in relation to your specific needs.

Buy-Sell arrangements can be structured in many different ways and you should always seek advice to ensure the rights and obligations contained in a Buy-Sell agreement reflect the wishes of the parties.

How do I get protected?

One of our financial advisers can help tailor the right cover for your needs.

Save yourself one less worry and contact one of our agents today.